A no-deal Brexit will sink the euro

The market assumption that a no-deal Brexit will be a much greater problem for the sterling than the euro is questionable. If Britain leaves the EU in March without an agreement there is an excellent chance it will be as costly for the euro and the Union as it has been for the sterling and the UK.

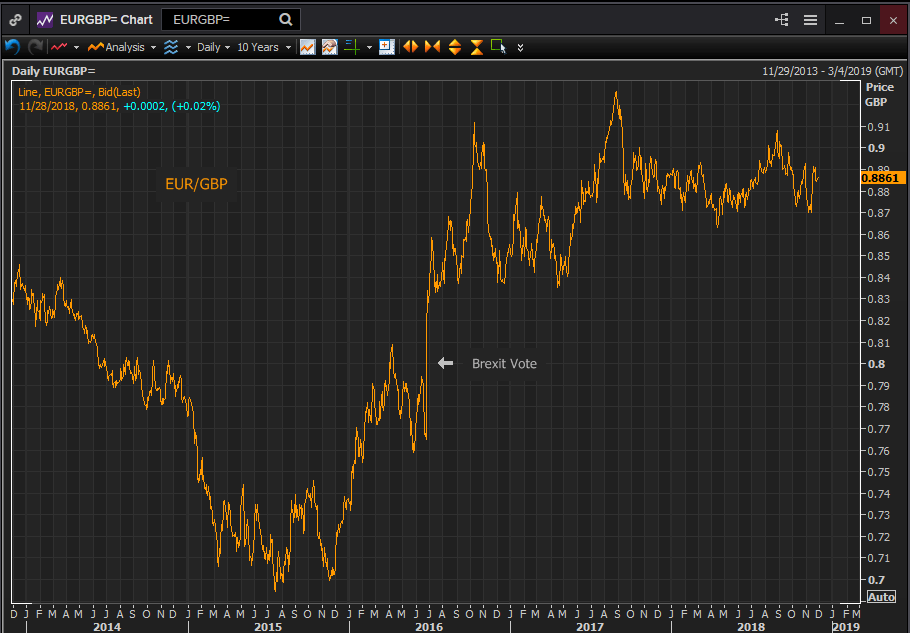

Sterling devaluation against the dollar has been almost double that of the euro. Since the June 24th 2016 referendum, the pound has lost 14.2% versus the euro’s 7.8%. Against the euro the pound has shed 15.8% in those two and one half years. A result commensurate with the disproportionate burden the UK economy is supposed to bear from the separation.

Britain sent £274 billion worth of goods and services to the EU in 2017 and imported £341 billion, according to UK data, giving the EU a £67 billion surplus with the UK. That EU trade is 44% of British exports.

The percentage of EU exports going to the UK as a part of the total depends on how you measure the Union's exports. If internal trade flows between EU countries are included along with non-EU destinations, then UK exports are only 8% of the bloc’s total. If however you count the EU as a unit and use only exports to countries outside the bloc as a base then UK exports are 18% of the total.

Trade between the EU and the UK is lopsided in percentage terms because of the comparison against the much larger economy of the 27 member European Union (excluding the UK), $16.0 trillion against the UK’s $2.8 trillion. Overall European Union exports without those of the UK were $5.28 trillion, those of the UK $442.1 billion. The EU population of 449.5 million is almost seven times that of the UK's 66.7 million.

The actual value of EU exports to the UK is 25% larger that the value of goods and services flowing East across the Channel though the EU economy is almost six times as large.

Still, however you cut it 44% of UK exports go to the continent while only 18% (at best) of EU foreign sales go west. That would appear to place a far heavier burden of separation on the UK economy. Markets have extracted that judgement from the sterling.

The almost universal assumption that the economic interdependence and the dangers of an unprepared exit would force a deal between the UK and the EU may yet be true. But it has made both sides complacent.

While it’s difficult to tell what has been done to prepare for a cessation of the existing trade, legal and financial arrangements, media coverage has been minimal. It is possible the bureaucrats have been busy planning for months. It is also possible that given the lack of direction from leaders who have been consumed with negotiations and the politics of the Brexit, little has been done. Considering the complexity and size of the task and the organizational drive necessary to accomplish it, the latter is far more likely

Even with the best case scenario for a non-deal exit, one that assumes both sides have elaborate contingency plans ready for March 30th, the disruption is bound to be monumental. While the worst case could see delays in the timely delivery of essential goods, medicines, food, and financial services. If the latest BMW 7 series cannot reach London no one will suffer, the same is not true for German pharmaceuticals or medical equipment.

Brexit’s trade disruption will fall exclusively on old line EU members. Of the UK's top ten trading partners, seven are from the EU. All are from Western Europe, in descending order of export value to the UK: Germany; France, Netherlands, Spain, Belgium, Italy, and Ireland. Their exports, premier marques, high added value and expensive, are the kind to have a heavy impact on an economy. Germany sends vehicles, machine tools, electronic equipment. France sends machinery, aircraft, vehicles and electronic equipment. The Netherlands machinery, electronics and refined fuels and Italy machinery, vehicles, pharmaceuticals and plastics.

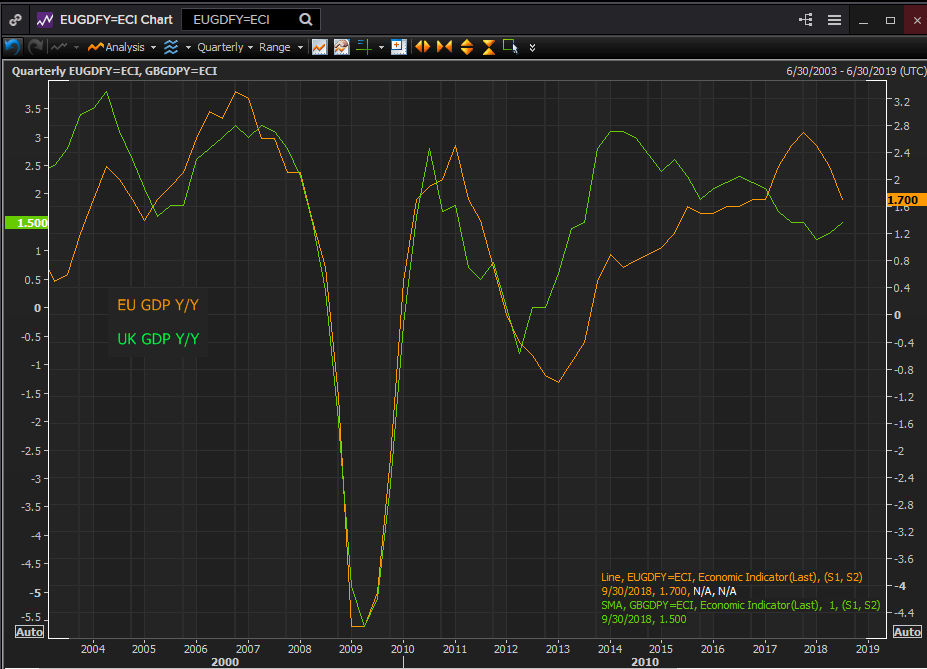

The EU grew just 0.2% in the third quarter. German GDP was negative, Italy was flat and France grew 0.4%. The effect of a large and immediate drop in their highest value exports will send the slowing EU economy into recession.

When the predictable effect of a no-deal Brexit on the EU economy is factored into the euro, the EUR/GBP will return to pre-referendum levels. The cross at 0.8100, its 2016 high before the vote, and the current sterling rate of 1.2795 would put the euro at 1.0325, 10 figures below its present level.

The electorates of Germany France and Italy are already dissatisfied with their governments, their political elites and Brussels. In Germany Angela Merkels’s Christian Democratic Union suffered its worst post-war defeat in the last election. Italy has elected the populist and euro-skeptic coalition of 5 Star and the League. France chose the never elected Emmanuel Macron.

If the intransigence of the EU Commission in the Brexit negotiations causes the UK to crash out of the EU, the resulting recession could cost the Union its strongest remaining supporters in Western European capitals. The Commissioners will not have preserved the Union, as they intended, but wrecked it.

Charts: Reuters

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.